Yuh Joint Account Review: Is Yuh&Me the Best Household Account in Switzerland?

- Flurin Bleisch

- 1 day ago

- 21 min read

Rent, health insurance, groceries or a holiday budget: shared expenses are often more complicated in everyday life than they need to be. With Yuh&Me, Yuh offers a free joint account with its own Swiss IBAN, TWINT, eBill, cards for both people and shared savings goals. Our hands-on test shows that, for managing shared everyday finances via an app, Yuh&Me is currently one of the strongest offers in Switzerland – provided both people trust each other and understand how a joint account works.

Welcome offer

CHF 50 Trading Credit + 250 SWQ

With the Yuh promo code YUHMON you get a CHF 50 trading credit and 250 Swissqoins on a minimum deposit of CHF 500.

The bonus applies to the personal Yuh account – not directly to the Yuh&Me joint account. Since both people need a personal Yuh account for Yuh&Me, both can use the promo code when opening their account and each benefit from the welcome offer.

Note: We are an independent Swiss financial platform. If you click on a link (affiliate link) or use one of our promo codes, we receive a commission from the provider – at no extra cost to you. Your account is opened exclusively with the provider; we do not receive any personal data. Our tests, reviews and rankings remain unaffected by this. Learn more

Table of Contents

The key facts at a glance

With Yuh&Me, Yuh offers a free, fully featured joint account for two people. It is well suited to couples, two-person flatshares, siblings or friends who want to organise shared expenses directly through a separate account.

Quick verdict: Yuh&Me is the strongest free joint account in Switzerland – above all because of the combination of a Swiss IBAN, TWINT, eBill, free cards and a clear separation between the personal account and the joint account.

Features: Its own IBAN, virtual and physical Mastercards, TWINT, eBill, real-time notifications and shared savings goals.

Costs: The personal Yuh account, the joint account and the associated cards are free. Fees mainly arise with frequent cash withdrawals, use abroad or currency exchange.

Requirements: Both people must be at least 18 years old, live in Switzerland and have a personal Yuh account. Marriage or a shared place of residence is not required.

Good to know: Both account holders can use the joint account individually. That's convenient, but it requires trust.

Not suitable for: Groups of more than two people. Yuh&Me is also less suitable if there isn't stable financial trust, or if you don't want to handle your banking solely via an app.

What is the Yuh&Me joint account?

The Yuh joint account is aimed at two people who want to manage their finances together. Typical examples are rent, electricity, internet, health insurance, insurance policies, groceries, travel, restaurant visits or shared purchases.

Yuh&Me does not replace your personal Yuh account, it complements it. Both people keep their own account with their own login and their own app. In addition, you both get a shared, fully featured bank account with its own Swiss IBAN, which is shown separately in the Yuh app. Yuh&Me is not intended for larger groups, as the account is limited to two people.

Shared expenses no longer have to run through one person's personal account. Instead, both can deposit money into the joint account or transfer it from their personal Yuh account, and manage shared bills, purchases or savings goals through it. What's shared runs through the joint account. What's private stays private.

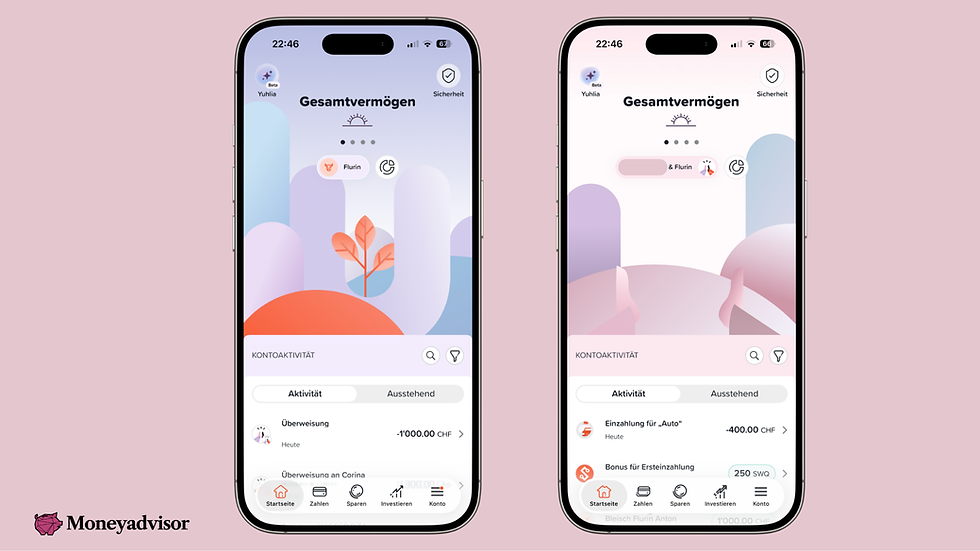

In our test, this very separation was one of the biggest advantages. With one tap you can switch between your personal account and the joint account. The app feels clear, modern and lively in typical Yuh style. The real-time notifications are practical too: both people immediately see what's happening on the joint account.

How switching between your personal account and the joint account works

Yuh has implemented the joint account very intuitively. On the home screen you switch between your personal account and the joint account with one tap on the name. It feels a little like switching between two profiles: in the personal area you're in your own financial world. In the Yuh&Me area you're in the shared financial world.

The two accounts are structured the same way – with a home screen, payments, saving, investing, cards and account settings. This keeps the app familiar, but the finances are neatly separated. Everything you do in the personal area affects your personal account. Everything you do in the Yuh&Me area affects the joint account.

The account transfer is also handy: money can easily be moved within Yuh from the personal account to the joint account, and back again if needed.

Opening the Yuh&Me joint account: this is how easy it should be

Opening the Yuh joint account is done directly in the Yuh app and is very simple. The requirement is that

both people have a personal Yuh account,

are at least 18 years old and

live in Switzerland.

Relationship status doesn't matter. So Yuh&Me isn't only intended for married couples; it's also suitable for unmarried couples, flatmates, siblings, friends or adult children with a parent. A shared place of residence isn't required either. That makes Yuh&Me more flexible than many classic partner-account offerings.

If both already have a Yuh account, opening it is quick. In our hands-on test, I set up the account together with my wife. The whole process – including the invitation, accepting the invitation, a brief review of the details by Yuh and digitally signing the contract – took less than 20 minutes. After that you just have to wait for Yuh to open the account. Our account was already set up the next day.

Welcome offer CHF 50 Trading Credit + 250 SWQ: If you don't have a Yuh account yet, you can use the Yuh promo code YUHMON when opening it. Since both people need a personal Yuh account for Yuh&Me, both can use the code and each benefit from the welcome offer. The bonus applies to the personal Yuh account, not directly to the joint account.

The process is straightforward: one person starts the opening in the app under "Account", answers a few questions about the relationship and the purpose of the account, and then invites the second person. That person accepts the invitation and also signs the contract digitally. Shortly afterwards, the joint account appears in the app alongside the personal account.

For a joint account, that's remarkably lean. Yuh reduces the process to just a few digital steps and makes opening it much easier than you'd expect from many classic joint accounts, where you usually have to go to a branch in person.

Who is the Yuh&Me joint account suitable for?

Yuh&Me is suitable for two people who want to easily organise regular shared expenses. That can be couples, flatmates, siblings or friends. Marriage or a shared place of residence isn't necessary; what matters is the shared financial everyday life.

The account is especially practical if both deposit a fixed amount each month and use it to pay rent, insurance, groceries, holidays or shared purchases. Instead of asking for money back via TWINT after every purchase or splitting bills at the end of the month, shared expenses can run directly through the joint account. That keeps things clearly separated: shared expenses run through Yuh&Me, private expenses through the personal account.

For larger flatshares, clubs or groups, however, Yuh&Me is not suitable. The joint account is limited to two people.

Debit cards, TWINT, eBill and a multi-currency account: everything shared finances in Switzerland need

A joint account is only really useful if it works in everyday life. What matters is whether it makes it easy to manage bills, card payments, TWINT and spontaneous expenses. This is exactly where Yuh&Me is particularly strong.

Debit cards

With the Yuh joint account, both people immediately receive a free virtual Mastercard linked to the shared balance. In addition, each person can order a physical Mastercard free of charge. In our test, the physical card for the Yuh joint account arrived in the mailbox on the second day after ordering. This means that up to four free Mastercards are possible for the same joint account: two virtual and two physical cards.

The separation is important: all Yuh&Me cards charge the joint account directly. Your private Yuh card stays separate and continues to charge your personal Yuh account. This lets you pay private expenses through your own account and shared expenses directly through Yuh&Me.

The cards can be used with Apple Pay, Google Pay or Samsung Pay. This lets you pay online, in store or on the go with your smartphone or smartwatch – even without a physical card.

What is a virtual card?

A virtual card is a digital debit card without a plastic card. It can be activated directly in the app and used for online payments or mobile payment (Apple Pay, Google Pay or Samsung Pay). The advantage: you don't have to wait for a physical card and can still pay directly from the right account.

A nice extra benefit is the Pocket Insurance. If certain everyday items such as a smartphone, laptop, keys, wallet or glasses are paid for with a Yuh&Me card, they can be insured at no extra cost. That's not a main argument for the joint account, but a practical advantage for shared purchases.

TWINT

TWINT is especially important in Swiss everyday life. Many shared expenses in Switzerland run through TWINT: at a flea market, at a children's clothing swap, at a club event or for a quick money transfer to friends. Since TWINT can be used with the joint account, the account becomes much more practical in everyday life.

In the Yuh TWINT app you can set in the settings whether your personal Yuh account or the Yuh&Me joint account is used by default for paying and receiving. When sending money, you can select which account is charged. This keeps you flexible about whether a payment is private or shared.

eBill

eBill is also an important point. My wife and I had already connected eBill beforehand via the sharing function; that basically works without a joint account too, directly through eBill. But the advantage with Yuh&Me is that shared bills can now be paid directly from the shared account.

Health insurance, insurance or other recurring bills no longer run through one person's personal account, but where they belong. That's one of the underrated advantages of Yuh&Me: the account doesn't just create a second IBAN, but a cleaner structure for shared finances.

Multi-currency account

Yuh is a multi-currency account, like the kind you know from Revolut. That means you can hold and manage several currencies such as Swiss francs, euros or US dollars separately within your Yuh account via a single IBAN.

At first that might sound more complicated than it is. For normal everyday use, you simply use the Yuh joint account in Swiss francs. Rent, health insurance, purchases, eBill, TWINT and most shared bills usually run in Swiss francs. You can ignore the other currencies if you don't need them.

The multi-currency account becomes practical above all when travelling, with online purchases in foreign currencies, or when you want to hold money together in euros or US dollars. For example, you can keep holiday money separately in another currency.

The only important thing is: if you exchange money, or if it has to be exchanged for a transaction in a foreign currency, Yuh charges a currency exchange surcharge of 0.95% on the interbank rate.

Transparency: both see what's happening

With Yuh&Me there is full transparency over the shared account. Both see which amounts come in, which payments were made and how shared savings goals are progressing. Card payments and transfers are also visible to both.

That can be very helpful in everyday life. You don't have to ask whether a bill has been paid or who covered the last purchase. Both see the same balance.

At the same time, you have to want transparency. Anyone who organises shared expenses gives the other person insight into this shared financial area. For couples or flatshares with clear rules, that's an advantage. For people who prefer to handle shared finances loosely and informally, it can feel too binding.

Yuh&Me doesn't automatically resolve money questions in relationships. But it ensures that shared expenses no longer disappear somewhere between personal accounts, TWINT payments and outstanding bills. What's shared becomes visible – and that's exactly what often makes everyday life more relaxed.

Shared savings goals

With Yuh&Me you can create shared savings goals, for example for holidays, furniture, a wedding, a move, larger purchases or a shared emergency fund.

The advantage lies above all in the overview: both can see at any time how close the goal already is and can add money. For short-term and medium-term goals, that's very practical, because the money stays clearly separated from the personal account.

For long-term wealth building, however, the savings goals are more of an organisation tool than an investment solution. Anyone who wants to build wealth together over the long term currently still needs a different solution. What's exciting, though, is that Yuh plans to enable joint investing in the future as well.

Costs and fees with the Yuh joint account

The Yuh joint account is permanently free. There is no monthly fee. Important: for the Yuh joint account, both people need a personal Yuh account – and that is free too. So there are no ongoing account management fees, either for the personal Yuh accounts or for the joint account.

There's no hidden cost trap with the cards either. Both the cards for the personal Yuh account and the cards for the joint account are free. The same fees apply to Yuh&Me as to a normal Yuh account. This makes the fee structure simple and transparent.

Service | Fee |

|---|---|

Account management, personal account + joint account | Free |

Virtual Mastercard | Free |

Physical Mastercard | Free |

Bank transfers within Switzerland | Free |

Cash withdrawal in Switzerland | 1 withdrawal per calendar week free, then CHF 1.90 |

Cash withdrawal abroad | CHF 4.90 per withdrawal |

SEPA transfer in EUR | Free |

SEPA transfer in another currency | CHF 4 |

Currency exchange | 0.95% surcharge on the interbank rate |

Interest on savings projects | 0% |

Customer service | Free |

For typical use as a household account in Switzerland, Yuh&Me can be used virtually completely free of charge. Shared bills, card payments, eBill, TWINT, Swiss transfers and savings projects work without a monthly fee.

Costs arise mainly with use abroad, frequent cash withdrawals or currency exchanges. In our view, this very cost structure is one of Yuh's biggest strengths: the basic offering is free, the fees are clear and arise mainly where actual additional costs occur. For shared everyday finances in Switzerland, Yuh&Me currently offers very strong value for money.

The Yuh joint account in the market comparison: why it's likely to be the best option for many

Yuh&Me doesn't stand alone in the market. Other banks and financial apps also offer solutions for shared expenses. Yuh stands out in particular because the joint account is free, integrated directly into the app and offers key functions such as its own IBAN, cards, TWINT, eBill and shared savings goals.

Provider | Model | Costs | Assessment | Opening |

|---|---|---|---|---|

Yuh&Me | Digital joint account for 2 people | CHF 0 per month | Very strong for anyone looking for a free app-based household account | Digital in the app |

neon duo | Digital joint account for 2 people | CHF 3 per person per month, card a one-off CHF 10 each | Good digital alternative, but not free | Digital in the app |

PostFinance partner account | Classic partner account within a banking package | depending on the package, e.g. Smart or SmartPlus from CHF 5 per month | Solid banking solution, but less lean and more expensive | Online + branch visit |

Swissquote joint account | Joint account with banking and shared trading | No additional costs for the joint account; normal Swissquote fees apply | Interesting for couples who want to invest and trade together | Directly in the app or on the web |

UBS me family/couple package | Comprehensive banking package | CHF 25 per month after the introductory phase | Good for advice and a comprehensive banking relationship, expensive for a pure household account | At the bank branch |

ZKB Banking | Classic banking solution | From CHF 6 per month, additional card from CHF 2 per month | Very strong classic alternative, but positioned less clearly than an app-based joint account | Online application or branch |

Zak shared pots | Expense management, between Zak accounts, but not a real joint account | free plug-in | Practical for splitting, but not a real shared account | Digital in the app |

neon duo

neon also offers a joint account for two people that is well integrated into the app. Unlike Yuh, however, neon duo is not free. For two people it costs CHF 6 per month, or CHF 72 per year. On top of that there are fees of CHF 10 each for the debit cards. Both people also have to live at the same address. Yuh&Me is more flexible here and, in our view, offers the more rounded Swiss everyday package with TWINT and the cards.

PostFinance partner account

With its partner account, PostFinance offers a classic solution. For the partner account there are two paid banking packages to choose from, Smart and SmartPlus. For existing PostFinance customers this can make sense if they want everything from a single source. But anyone looking for a modern, inexpensive and digital household account will find a more direct solution with Yuh. In addition, Yuh also offers a personal account directly and for free, whereas with PostFinance that would come at an extra cost on top.

Swissquote joint account

Swissquote is Yuh's parent company. The two offerings pursue different goals, however: Yuh&Me is the simple solution for shared everyday finances, while the Swissquote joint account is geared more towards joint banking, trading and wealth building. Anyone who mainly wants to organise rent, purchases, bills, TWINT payments and shared savings goals is better served by Yuh&Me. Anyone who instead wants to invest, trade or build a shared portfolio together will find the more suitable solution within the same banking group in the Swissquote joint account.

UBS me banking package for families and couples

UBS positions its offering more as a banking package for families and couples. That's interesting if you want several accounts, cards, advice and a comprehensive banking relationship. For a pure household account, however, it's considerably more extensive and more expensive than the Yuh joint account.

ZKB

At Zürcher Kantonalbank you can also open the paid banking packages (Silver, Gold, Platinum) as a joint account. The partner card then also costs an additional monthly fee. The difference isn't only about the price, but also about the product experience. Yuh&Me is clearly built as a shared app account for two people. With ZKB it's more of a classic account with joint account management.

Zak shared pots

Zak from Bank Cler is only partly comparable. The shared pots help to record, split or keep an eye on expenses together. But they aren't a real joint account with its own shared IBAN, card logic and joint account management. For travel, groups or loose settling-up, Zak can be practical. But anyone looking for a fully featured shared household account will find the more suitable solution with Yuh&Me.

Why Yuh is making a statement in the market with the joint account

Yuh didn't invent the joint account. But Yuh has consistently conceived it as a shared app account. At many classic banks, a normal account legally becomes a joint account. That works, but often doesn't feel like a product developed specifically for shared finances. Yuh&Me feels different: its own display in the app, shared cards, TWINT, eBill, savings goals and a clear separation from the personal account. On top of that, there's no monthly fee and no requirement such as marriage or a shared place of residence. It's exactly this combination that makes Yuh&Me especially attractive for many couples, friends, siblings and two-person flatshares.

The most important insight: Yuh&Me is a trust product

The Yuh joint account makes shared finances easier. But like any real joint account, it requires trust. Both account holders can use the account individually. For payments, transfers or money movements, no consent from the other person is generally needed.

In everyday life that's practical. A household account would be of little use if every payment had to be approved twice. At the same time, it also means: anyone who opens Yuh&Me gives the other person genuine ability to act on shared money.

This becomes especially important with larger amounts. Just because two people have joint access to an account doesn't automatically clarify who economically owns which share. It's therefore worth setting down simple rules: who pays in how much? What is the account used for? How is a balance divided in the event of a separation, closure or dispute?

Financial clarity isn't mistrust. Particularly with shared finances, it's often the prerequisite for the account to work smoothly in everyday life.

What happens in the event of a dispute, closure or death?

A joint account doesn't just have to work in the normal case. Difficult situations should also be understood before opening it.

If a dispute or conflicting instructions arise between the account holders, Yuh can take protective measures. This can include the account being frozen in whole or in part, instructions not being carried out, or both people having to act jointly. In a separation or in the event of serious conflicts, in the extreme case this can mean that the balance temporarily cannot be freely used until a court settles the dispute.

The account closure should also be understood. According to the terms and conditions, any joint account holder can request closure. If there are no clear or complete instructions, Yuh can retain the balance until it's been clarified where it should be transferred.

In the event of the death of an account holder, the heirs can be informed of the existence of the joint account. After that, it can become relevant which share of the balance belongs to the estate. Particularly with larger amounts, you should therefore not rely on the app logic alone, but document the economic allocation properly.

Our recommendation: Use the Yuh joint account above all as a household account for ongoing expenses and clearly defined savings goals. For large assets, inheritances, house building, education costs or other larger money movements between partners, proper documentation is always worthwhile. The joint account is no special case here; it just makes shared money flows more visible and more binding.

Security and deposit protection

Yuh's banking services are provided by Swissquote Bank Ltd, to which Yuh also belongs. This means the money is held at a Swiss bank that is subject to FINMA. That's an important security difference compared with many foreign financial apps.

For deposit protection, the personal accounts and the joint account have to be considered separately. The balance on each personal Yuh account is protected separately up to CHF 100,000. In addition, the Yuh&Me joint account is treated as its own customer relationship and, as a joint holding, is likewise protected up to a total of CHF 100,000. The important point is: with the joint account, this limit applies to the joint holding as a whole and not per person. For normal household expenses and shared savings goals, that's usually sufficient.

What Yuh&Me can't do (yet)

Yuh&Me is currently not a shared investment account. Investing is currently only possible via personal Yuh accounts. Yuh does point out that this function is being worked on, but for now you shouldn't plan Yuh&Me as a solution for joint investing.

Several joint accounts or more than two account holders aren't possible either. Per duo, the offering is limited to one joint account. Yuh is also an app-based solution. Anyone who prefers personal advice in a branch, paper processes or a classic banking relationship may be better off with a traditional bank.

Pros and cons at a glance

Pros

Yuh&Me is free and offers strong value for money.

Opening the account is very simple and was quickly done in our hands-on test.

Personal and shared finances stay cleanly separated.

The combination of a Swiss IBAN, TWINT, eBill, cards and savings goals is well suited to everyday life.

Both people have full transparency over shared payments.

The account is very well suited to couples and two-person flatshares.

Cons

The account is only available for two people.

Joint investing isn't possible yet.

In the event of a dispute, separation or death, legal and practical questions can arise if the division isn't clearly settled.

For large balances or unclear ownership situations, Yuh&Me is less suitable.

Anyone who wants branch advice is better off with a classic bank.

Conclusion: the best joint account for many couples and flatshares

In our hands-on test, the Yuh joint account impresses with its simple opening, clear app integration and the strong free basic offering. The combination of its own Swiss IBAN, TWINT, eBill, cards for both people, shared savings goals and a clean separation between the personal account and the joint account is particularly well done.

In the market comparison, Yuh&Me is the strongest offering for shared everyday finances.

neon duo is a good digital alternative, but charges a monthly fee. Within the same banking group, Swissquote is the more suitable solution when joint banking, trading and wealth building are the priority. PostFinance, ZKB and UBS are more classic banking packages, while Zak does help with splitting but isn't a real joint account.

This makes Yuh&Me especially interesting for couples, two-person flatshares, siblings or friends who want to manage shared expenses simply, digitally and free of charge. But one thing remains important: the joint account works like a trust product. Both people can use the shared balance. Particularly with larger amounts, there should therefore be clear arrangements on who pays in how much and who economically owns which share.

Our recommendation: anyone looking for a lean household account via an app who doesn't need branch advice will find in Yuh&Me the most convincing joint account in Switzerland. Anyone with larger assets, complex ownership questions or no stable financial trust should take a closer look before opening it to see whether a joint account is the right solution.

Welcome offer

CHF 50 Trading Credit + 250 SWQ

With the Yuh promo code YUHMON you get a CHF 50 trading credit and 250 Swissqoins on a minimum deposit of CHF 500.

The bonus applies to the personal Yuh account – not directly to the Yuh&Me joint account. Since both people need a personal Yuh account for Yuh&Me, both can use the promo code when opening their account and each benefit from the welcome offer.

Note: We are an independent Swiss financial platform. If you click on a link (affiliate link) or use one of our promo codes, we receive a commission from the provider – at no extra cost to you. Your account is opened exclusively with the provider; we do not receive any personal data. Our tests, reviews and rankings remain unaffected by this. Learn more

FAQ

What is the Yuh&Me joint account?

Yuh&Me is an additional account for two people. Both keep their personal Yuh account and additionally get a shared account with its own Swiss IBAN. This can be used for shared expenses, bills, payments and savings goals.

Is the Yuh&Me joint account free?

Yes. The Yuh&Me joint account has no monthly fee. The associated cards are free too. For certain services, however, the normal Yuh fees apply, for example for cash withdrawals abroad or currency exchange.

Who can open a Yuh&Me joint account?

The joint account can be opened by two people who both live in Switzerland, are at least 18 years old and have an active personal Yuh account. A shared place of residence or a particular relationship, such as marriage or partnership, is not required.

Can both people use the account freely?

Yes. Both account holders can use the joint account individually. For payments, transfers or other transactions, no consent from the other person is generally required. That's why a joint account should only be opened with someone you trust financially.

Are personal and shared finances separated?

Yes. The personal Yuh account and the Yuh&Me joint account stay separate from each other. In the Yuh app you can switch between your personal account and the joint account. This lets you manage shared expenses without mixing them with personal finances.

How do you open the Yuh&Me joint account?

Opening is done directly in the Yuh app. Both people need a personal Yuh account, their own device and their own login details. One person starts the opening (go to the "Account" area and then select "Open joint account"), invites the second person, and both sign the contract digitally. After that, the joint account is opened.

How can the joint account be closed?

Any account holder can request closure of the joint account at any time and without the consent of the other joint account holder. If there's no clear instruction on transferring the balance, Yuh can retain the balance until it's been clarified where it should be transferred.

What happens in the event of an account holder's death?

The surviving joint account holder can continue to use the account. Yuh informs the heirs of the existence of the joint account. It must then be determined whether and which share of the balance falls into the estate.

How do you tax a joint account?

In principle, assets and interest income have to be taxed by the person to whom the balance economically belongs. For married couples, the account is declared in the joint tax return. For unmarried couples, siblings, friends or flatmates, it should be internally clear who holds which share of the balance.

Is Yuh&Me an OR account or an AND account?

Yuh&Me works like an OR account. This means: both account holders can use the joint account individually. For payments, transfers or other money movements, no consent from the other person is generally needed.

With an AND account, by contrast, both people would have to agree jointly before the account could be used. That offers more control, but would be considerably more cumbersome for an everyday household account. Yuh&Me therefore relies on the practical OR logic – and thus also on mutual trust.

Is there a welcome offer for the Yuh&Me joint account?

The Yuh promo code YUHMON doesn't apply directly to the Yuh&Me joint account, but to the personal Yuh account. Since both people first need a personal Yuh account for Yuh&Me, both can use the promo code when opening their account and each benefit from the welcome offer. The bonus is allocated to the personal Yuh account, not the joint account.